What Small Business Owners Need to Know About Health Plans and IT Risk

Small business leaders and IT teams should review how the 2027 NBPP proposed rule will change employee health plans, compliance requirements, and data security.

The 2027 NBPP proposed rule, issued February 11, 2026, will reset key rules for ACA Exchanges and small‑group health plans starting in 2027. As a small or mid‑sized business owner, these changes affect your benefit strategy, your HR workload, and the IT systems that support them.

Big Picture: What’s Changing

Catastrophic and some bronze plans can carry significantly higher out‑of‑pocket maximums, shifting more financial risk to employees.

CMS proposes multi‑year catastrophic plans and broader hardship exemptions, making catastrophic coverage more common among workers who cannot or do not enroll in richer plans.

Agents, brokers, and web‑brokers must use standardized HHS‑approved consent and eligibility review forms, creating more structured documentation.

Certain state‑mandated benefits will be treated as “in addition to” Essential Health Benefits, affecting plan design and cost structure.

Concrete Action Steps for Owners and IT

For the business owner/CEO:

Reevaluate your health benefits package

Ask your broker which 2027 plan designs they expect to offer and whether your team could be pushed toward higher‑OOP bronze or catastrophic options.

Model the total compensation impact if benefits become less generous and consider offsetting with stipends, HRAs, or plan upgrades.

Upgrade HR policy and employee education

Provide clear, written explanations of how deductibles, out‑of‑pocket maximums, and catastrophic coverage work under the new rules.

Set expectations about documentation employees should keep (especially standardized federal consent and eligibility forms tied to subsidies).

For your IT department or MSP:

Prepare your systems for new standardized forms and proofs

Ensure HRIS, payroll, and document systems can accept, tag, and secure HHS‑approved consent and application review forms your broker will use.

Build simple workflows for HR to retrieve this documentation during audits, disputes, or employee questions.

Tighten security around benefits and PHI‑adjacent data

Implement strong identity and access management, encryption, logging, and vendor controls for any system that touches health coverage or subsidy information.

Confirm that contracts with benefits platforms, brokers’ portals, and HR tools reflect updated privacy and security expectations.

Likely Employee Questions – And How to Answer

“Why did my maximum out‑of‑pocket jump so much?”

Under the 2027 NBPP, some bronze and catastrophic plans are allowed to exceed prior out‑of‑pocket caps, which can significantly increase your financial exposure if you get sick or injured.

“What are these new standardized forms from the broker?”

Federal rules now require standardized HHS‑approved consent and eligibility review forms to document the accuracy of your application and protect your subsidy eligibility.

“Are all state‑mandated benefits still fully covered?”

Not always; certain state‑required benefits are treated as outside the core Essential Health Benefits package, which may affect how they’re funded and covered.

How Farmhouse Networking Helps SMBs

Farmhouse Networking partners with small and mid‑sized businesses to turn regulatory change into structured, low‑friction processes:

Integrate new federal consent and eligibility documentation into your HR and document‑management stack, so HR can find what they need in seconds.

Implement or enhance cybersecurity controls around benefits, payroll, and identity data to reduce risk as health coverage documentation becomes more standardized and audit‑friendly.

Coordinate with your broker and benefits platforms so technical changes (new forms, new plan designs) are reflected cleanly in your systems with minimal disruption.

Call to Action Email support@farmhousenetworking.com to get a focused assessment of how the 2027 NBPP proposed rule intersects with your benefits, IT, and employee experience – and a concrete plan to get ahead of it.

Small business owners should update ownership records and IT controls to align with FinCEN’s new due diligence relief and banking compliance requirements.

FinCEN has issued an order granting relief from part of its Customer Due Diligence rule, so banks no longer must re‑identify and re‑verify beneficial owners every time your company opens a new account or product. Instead, they focus ownership checks on initial account opening, when something about your information looks off, and when their risk‑based procedures say they should dig deeper.

The Core Change in Simple Terms

Under this exceptive relief, your bank must confirm your company’s beneficial owners only:

At the first account opening with that institution.

When they learn facts that call your existing ownership information into question.

As needed under their ongoing risk‑based due‑diligence procedures.

They are no longer required to repeat the beneficial ownership process for each subsequent checking account, loan, or credit card you open with them.

Concrete Steps for Owners and IT

Owner/management actions:

Keep ownership data clean: Maintain a current list of all beneficial owners (and key controllers) with legal names, tax data, and ownership percentages so you can certify accuracy quickly when requested.

Align with your bank: Ask your relationship manager how they will apply the relief, what they will still ask for, and how your internal records can make their reviews faster.

Tie into CTA/BOI: If your company is subject to beneficial ownership reporting, ensure your BOI filings, internal records, and the bank’s records are consistent.

IT department actions:

Centralize and secure records: Store ownership documents, formation records, and signatory forms in a secure repository with encryption, permissions, and audit logging.

Implement change‑management: Put in a formal process so every ownership change, equity issuance, or leadership change creates an IT and compliance ticket to update records and access rights.

Protect financial access: Enforce MFA, least‑privilege access, and monitoring on all systems connected to banking, payments, and accounting, supporting the bank’s risk‑based oversight with strong internal controls.

Common Customer Questions (and Answers You Can Use)

“Is my business still being monitored for suspicious activity?” Yes. The relief removes duplicated paperwork but does not change the Bank Secrecy Act’s risk‑based monitoring and reporting framework.

“Will my bank ask for less paperwork now?” In many cases, yes, especially when opening additional accounts or services with the same institution, because they can rely on previously collected ownership information when appropriate.

“Do I still need to tell my bank when ownership changes?” Absolutely. If the bank discovers that ownership data is outdated or inaccurate, they must revisit their due diligence, and delays or risk re‑assessment may follow.

How Farmhouse Networking Helps SMBs Turn Relief into Advantage

Farmhouse Networking helps small and midsize businesses convert regulatory changes into operational improvements by:

Designing secure, centralized systems for ownership, governance, and banking documentation.

Automating workflows triggered by ownership and leadership changes to keep systems, access, and records aligned.

Strengthening IT security around financial systems so your risk profile stays low while your bank leans more on a risk‑based approach.

To learn how to implement these steps efficiently and securely, email support@farmhousenetworking.com for more information about how Farmhouse Networking can help improve your business.

Small business leaders should review AI assistant security settings with their IT team to protect customer data and reduce cybersecurity risks.

Every department in your company is experimenting with AI assistants for drafting emails, analyzing documents, and answering questions—but mis‑sharing data with these tools is rapidly becoming a top cybersecurity concern. As the business owner, you need AI productivity without turning your data into the next breach headline.

Key security risks with online AI assistants

Employees paste sensitive data (contracts, passwords, customer lists, financials) into public AI tools, creating uncontrolled copies outside your security perimeter.

AI agents that connect to email, CRM, and file shares can over‑index data and ignore internal permissions, exposing information to users who should not see it.

Shadow AI—unapproved tools adopted by teams—means no vendor vetting, no logging, and no consistent security controls.

Mis‑configured orchestration and weak authentication give attackers new ways to abuse AI agents to access systems and data.

Action plan for you and your IT team

Define an AI usage policy

Specify what data is never allowed in public AI (customer PII, financials, credentials, trade secrets).

List approved AI tools, who may use them, and for what business cases, and require IT review for any new AI platform.

Harden AI tools technically

Enforce single sign‑on, multifactor authentication, and role‑based access to AI assistants tied to your identity platform.

Configure least‑privilege access to email, CRM, and file systems and enable audit logging for AI actions and data access.

Monitor, train, and prepare for incidents

Monitor for unsanctioned AI usage and phase in secure alternatives.

Train staff on safe prompting habits: strip identifiers, avoid secrets, and use internal assistants where possible.

Update your incident‑response plan to include AI mis‑sharing, compromised AI accounts, and vendor‑side issues.

How to answer customer questions

“Are you putting our data into ChatGPT?”

“We only use AI within secure, approved platforms, and we prohibit staff from pasting your identifiable information into public AI tools.”

“Could your AI assistant leak our information?”

“We enforce strict access controls, logging, and vendor security requirements to prevent unauthorized access or cross‑customer exposure.”

“What happens if something goes wrong?”

“We have a defined response plan that includes containment, investigation, and transparent communication if an AI‑related incident affects your data.”

How Farmhouse Networking can help SMBs

Farmhouse Networking can assess where AI is already in use across your environment, identify the highest‑risk workflows, and recommend safer, governed alternatives. We help you implement secure AI architectures, policies, and training so your team can adopt AI confidently while keeping customer data, intellectual property, and compliance obligations under control.

Email support@farmhousenetworking.com for more information about how Farmhouse Networking can help improve your business and secure AI use.

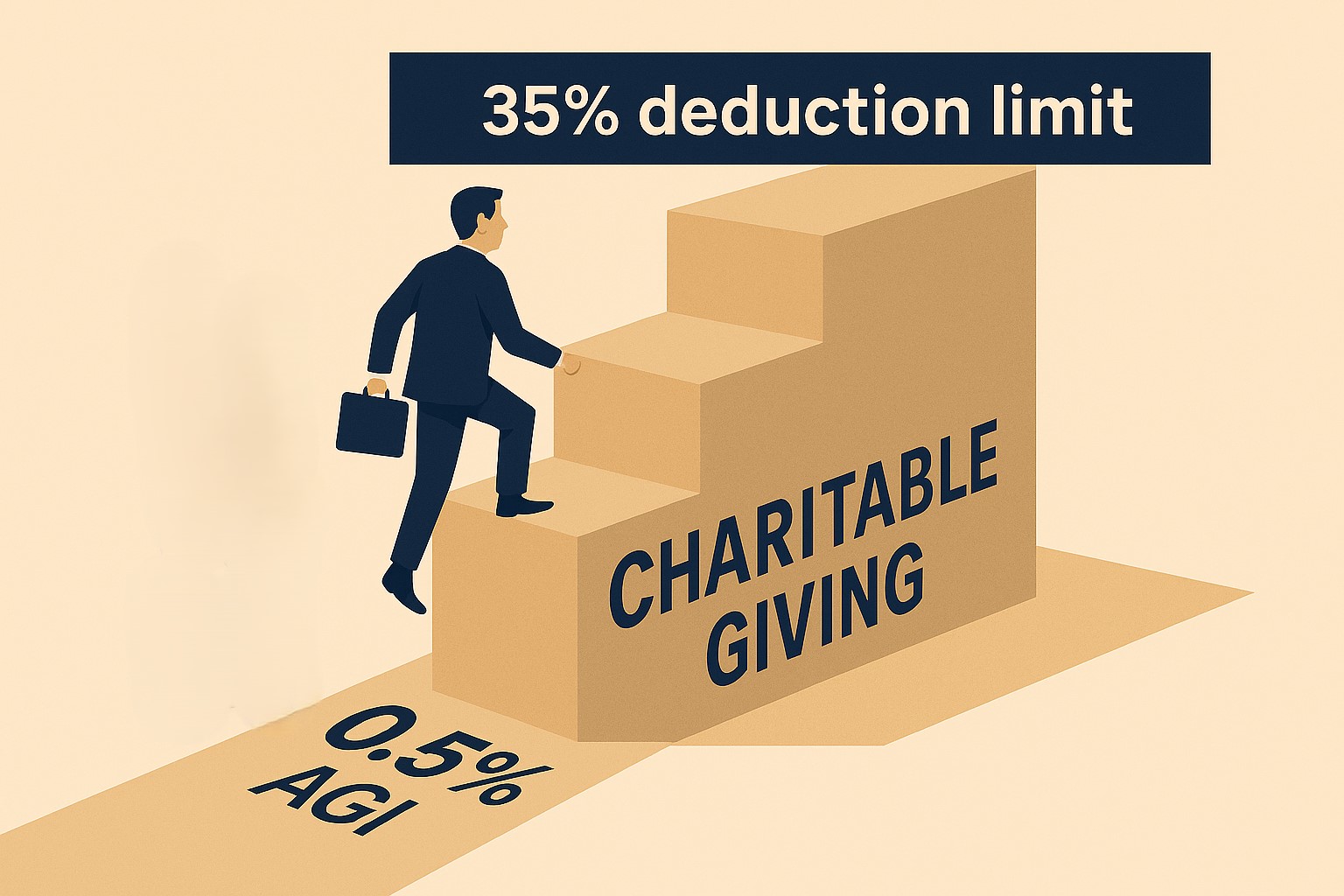

Small business owners can use clear reporting and documentation systems to navigate 2026 charitable giving rules and maximize tax‑deductible donations.

If your business donates to local nonprofits, schools, or community projects, the 2026 charitable giving rules change how much of that generosity you can deduct. The mechanics are more complex, but with the right systems you can still give strategically and get the full benefit available.

What Changed for Small Businesses in 2026

Your corporation can now deduct charitable contributions only to the extent they exceed 1% of taxable income, and total deductible contributions are still capped at 10% of taxable income, with excess potentially carried forward up to five years.

As an individual owner, your personal deductions are subject to a 0.5% AGI floor, though cash gifts to qualifying public charities remain deductible up to 60% of AGI.

A new, permanent charitable deduction for non‑itemizers lets individuals deduct up to $1,000 (single) or $2,000 (joint) for qualifying gifts starting in 2026.

All of this sits on top of existing substantiation rules: written acknowledgments for gifts of $250 or more and additional requirements for non‑cash contributions.

Action Steps for Owners and IT Teams

For the business owner:

Revisit your giving strategy:

Identify how much you typically give each year and whether it clears the new 1% floor and stays within the 10% cap for corporate deductions.

Coordinate with your tax advisor:

Decide whether to increase or bunch certain donations into specific years so you actually realize the deductions you expect.

Clarify business vs. personal giving:

Separate corporate contributions from personal donations so both you and your company can plan around the new floors and limits.

For your IT or technical team:

Build a clear digital trail:

Implement structured storage for donation receipts and acknowledgments, linked to accounting entries and accessible for your CPA during tax season.

Standardize data and approvals:

Use simple forms or workflows where staff record donation details—amount, date, charity, purpose, and whether any benefits were received—before payments go out.

Security and retention:

Protect donor‑related and financial data with proper access controls and keep records long enough to support the five‑year carryforward window for excess contributions.

Questions Your Customers or Community Partners May Ask

“Is my company’s sponsorship of your event still tax‑deductible?”

It may be treated as a charitable contribution or as advertising/marketing depending on the benefits received; in either case, new floors and caps can affect the deduction.

“Does it still help me tax‑wise if I give small amounts?”

Smaller gifts may not exceed the new floors by themselves, which is why many taxpayers will see more benefit from fewer, larger, or more concentrated gifts.

“Why do you need to send such detailed receipts?”

The IRS requires specific elements in acknowledgments for gifts of $250 or more and for non‑cash donations, so detailed receipts protect both you and your donors.

How Farmhouse Networking Supports SMBs

Farmhouse Networking helps small and mid‑sized businesses turn charitable giving from an ad‑hoc expense into a well‑tracked, well‑documented, and strategically planned process. We integrate your accounting tools with secure document management, create simple digital forms for recording donations, and set up dashboards so you can see where you stand relative to the 1% floor and 10% cap.

We also support customer‑facing communication—website content, FAQs, and email updates—so your community partners understand that you are still committed to giving, and how the 2026 rules affect them.

Email support@farmhousenetworking.com to find out how Farmhouse Networking can help your business modernize its systems and make smarter, more strategic charitable giving decisions under the new 2026 regulations.

And God will generously provide all you need. Then you will always have everything you need and plenty left over to share with others. As the Scriptures say,

“They share freely and give generously to the poor. Their good deeds will be remembered forever.”

For God is the one who provides seed for the farmer and then bread to eat. In the same way, he will provide and increase your resources and then produce a great harvest of generosity in you. - 2 Corinthians 9:8-10

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.